The monthly payroll scramble: How to end it

Every founder dreads payroll. Here's how to automate it and turn 30 minutes into 3.

February 16, 2026

Sean Mullaney

~5 minutes read

The monthly payroll scramble: How to end it

Payroll happens every month, whether you're ready for it or not. Your team needs to get paid. But to your banking app, payroll is just a series of random transfers. Your bank has no idea you're paying your team. It doesn't know this happens monthly. It doesn't know it's time-sensitive. It isn’t designed to support payroll, so you end up doing it manually.

We built payroll into Seapoint because your business account should be able to handle the regular financial processes you actually need to run, not just store money.

Sound familiar? How most founders run payroll

Your accountant does the hard part. They handle all the gross-to-net calculations, all the edge cases - someone wants bike-to-work, another person's on maternity leave, pension contributions change, tax codes adjust. They send you a PDF with the final numbers.

Then it's your turn. You manually pay each person: copy the amount from the PDF, paste into your banking app, verify with 2FA, next person.

Thirty minutes later, if you're lucky, you're done.

One founder described their setup: "Sales commission data feeds from one spreadsheet into a commission report, which gets manually transferred into the payroll Excel sheet. That gets sent to the accountant, who processes it and sends back a bank file. Then I upload that to my business account for bulk payment." Their verdict? "It's very convoluted. It's bonkers to me."

And you do this every month.

The real cost

The time adds up. But the real cost is the context switch.

Most banks won't let you schedule these payments ahead. You have to do it on the day. So you set a calendar reminder. You might be in a product meeting or on a customer call, but whatever you're doing has to stop.

Then there's the anxiety of hitting limits. One founder told us about constantly requesting temporary payment increases for payroll, increases that can take days to approve. Another described hitting their monthly outflow limit on payroll day, unable to reach a person to help resolve it. Your team is waiting to get paid, and you're stuck.

New employee joined mid-month, did the accountant include them? Someone left, did you remove them? Expense reimbursements need adding, where's that sheet?

It's extremely boring and stressful.

Why payroll software doesn't help

Platforms like BrightPay and Sage pitch self-service payroll - you can handle it yourself, no accountant needed.

These tools work fine when everything is typical. But as soon as there's an edge case, e.g. someone goes on maternity leave, wants to adjust their pension, or has a tax code change, you're digging through the software trying to figure it out.

You've removed the human expert from the loop - your accountant. It all falls on you. Get it wrong, and you're explaining to your team why their payslip is incorrect. That's scary.

Accountants charge under €100/month for payroll. It's a loss-leader to get your accounting business. Every founder I’ve encountered wants that safety blanket.

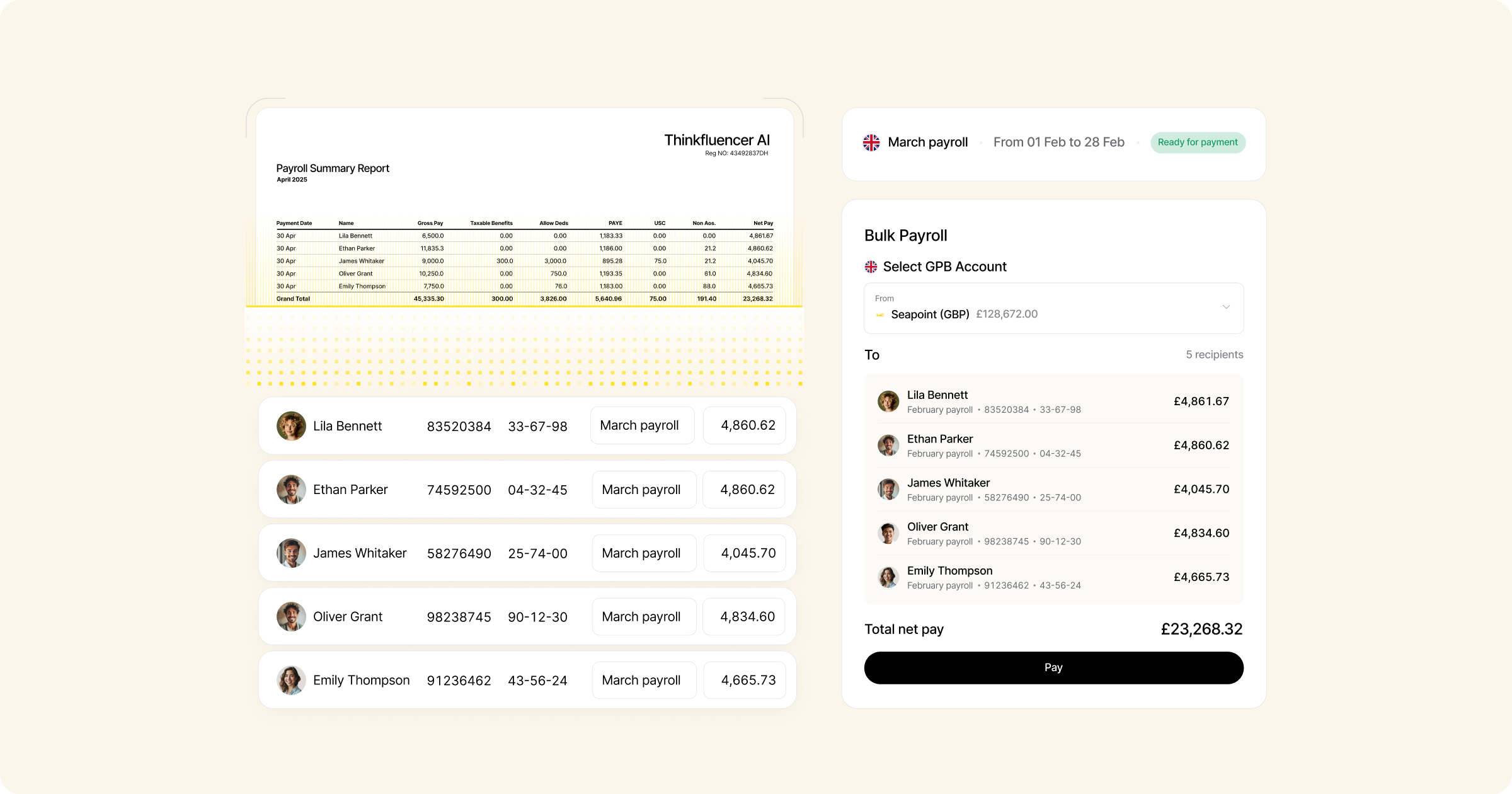

How Seapoint automates the execution layer

Seapoint is not trying to replace your accountant. Here's what we realised: payroll is a three-party process. Your employee needs to get paid. Your accountant needs to calculate it. You need to approve and execute it. But everyone's working in isolation - spreadsheets, email, PDFs flying back and forth. You become the integration layer, manually stitching it all together.

Seapoint is the collaboration space that should have always existed.

Employees onboard themselves. When someone joins your company, they log into Seapoint and provide everything needed for payroll - IBAN, tax details, birthday, address. They're onboarded to payroll without the founder collecting information through email or Google Forms.

Accountants are first-class citizens. Your accountant logs into Seapoint, sees up-to-date information for everyone, runs the payroll calculations, uploads the payslips, and sends them to the founder for approval. No more emailing PDFs. No more hoping the information is current.

Founders review and schedule. You see the payroll your accountant prepared, review it, approve it, and schedule it to run on the 26th (or whenever). Weekend or bank holiday? Seapoint adjusts to the preceding weekday automatically. You can be on a flight and payroll still runs. You don't have to remember. You don't have to be available. It just happens.

Employees get their payslips instantly. Everyone logs in, sees their payslip, knows they're getting paid. No more forwarding PDFs. No more "did you get it?" messages.

Three minutes instead of thirty. No spreadsheets. No email ping-pong. No manual copying. Just a collaboration space where everyone has their role and the process actually works.

One Seapoint customer put it: "Importing our payees was super straightforward, and now that everything's set up, running weekly payroll is much quicker and easier."

Before and after

Before:

- Accountant emails PDF on the 24th

- Set reminder for the 26th

- On the 26th, drop everything

- Manually enter each payment for 30 minutes

- Hope you don't hit a payment limit

- Hope nothing breaks

With Seapoint:

- Employee onboards themselves when they join

- Accountant prepares payroll in Seapoint with current info

- Founder reviews and schedules in 3 minutes

- Payments go out automatically on schedule

- Everyone gets their payslip instantly

The same workflow handles contractor invoices, employer-of-record bills from Remote or Deel, and vendor payments. Upload, review, schedule, done.

As another founder said: "I'm excited. It feels like I have a bird's-eye view of everything, along with some controls and actions I can take. When it comes to paying bills and payroll, this is immediately going to be a big win."

We're rolling out the full collaboration features over the next few months. The foundation - AI payroll processing, bulk payments, and scheduling - is live today.

If you're tired of being the integration layer between your team, your accountant, and your bank, open a Seapoint account.

Your startup triggers fraud alerts: Why the banking system fails founders

Banks can't tell startups from fraud: Learn why VC-backed founders face rejection, frozen accounts, and endless KYB - and what needs to change.

February 4, 2026

Sean Mullaney

~5 minutes read

Your startup triggers fraud alerts: Why the banking system fails founders

Here's what raises red flags for a bank:

- A newly incorporated company

- One or two individuals who own the entire thing

- No trading history

- No revenue

- No customers

- A sudden large capital injection from an offshore jurisdiction

- Directors in multiple countries

Now here's what a seed-stage startup looks like:

- A newly incorporated company

- One or two founders who own the entire thing

- No trading history

- No revenue

- No customers

- A funding round from a VC fund (domiciled in the Caymans, Luxembourg, or Delaware)

- A distributed team

The compliance system can't tell the difference. And honestly? It's not trying to.

The Opt-out

When Starling Bank got fined by the FCA for inadequate anti-money-laundering procedures, they had two options: fix the procedures, or stop serving the customers that triggered them.

They chose the second. Rather than figure out how to assess higher-risk accounts properly, they stopped onboarding them and offboarded the ones they had. Just like that.

This isn't an outlier. It's the logical response to a cost structure that makes certain customers unprofitable to understand. Legacy banks have compliance costs that run into the hundreds per account. Meanwhile, neobanks have automated everything so aggressively that their KYB costs have to stay low to make the economics work - large teams processing accounts at speed with no room for judgement calls.

When you're a VC-backed startup, you don't fit either model. You're too expensive for the legacy banks to bother with, and too weird for the neobank checklist. So you get rejected, frozen, or ground down by process until you eventually get through - weeks or months later - or stitch together some combination of accounts that technically works but wastes hours of your time every month.

The banks aren't confused about what you are. They just don't have a way to serve you that makes sense for them. And if they could choose not to serve you at all, they probably would. They just can't say that out loud.

One due diligence after another

Here's what makes this absurd - if you've raised venture capital, you've already been through one of the most rigorous due diligence processes that exists.

A lead investor will spend months investigating you. They'll call your old boss. They'll talk to founders you worked with ten years ago. They'll hire lawyers to comb through your cap table and accountants to stress-test your projections. Why? Because they're putting their fund's money and their own reputation on the line.

Then you go to open a bank account and someone asks if you have a website yet.

I mean, think about it. You've just survived three months of a VC tearing apart every assumption in your business. And now you're filling out forms designed for someone opening a sandwich shop.

Banks don't recognise VC funding as a signal of legitimacy. Their systems can't parse it. So they duplicate the process (badly) with forms designed for small businesses and risk models that can't process a cap table. You end up having to prove yourself all over again: once to investors who understand what they are looking at, and again to compliance teams who don't. Most startups have more than one bank account - as they should - so they find themselves going through due diligence processes again and again.

The safety theatre

Founders often assume that traditional banks are at least safer. The deposit insurance. The regulatory oversight. The implicit guarantee that comes with banking at an institution that's "too big to fail."

The reality is less reassuring.

Deposit insurance in most European countries covers €100,000. That's it. If you've raised a seed round, that's a fraction of what's sitting in your account. The rest is protected by the bank's balance sheet, which, as SVB demonstrated, can evaporate over a weekend.

And even when deposit insurance does apply, accessing it isn't instant. In a bank failure, funds get frozen while regulators sort through creditors and determine who's owed what. That process can take months. Six months. Maybe longer. If you're a startup that needs to make payroll next week, "you'll eventually get your €100k back" isn't much comfort.

The security that founders think they're getting from traditional banks is largely theatre. The real question isn't whether your bank has a licence, it's whether you understand where your money actually sits and how quickly you can access it whenever you need to.

What banks could see (if they understood)

The alternative isn't lower standards. It's different standards.

If someone has raised from a reputable VC, that's a signal. If they've already passed KYB at HSBC and you can verify it through open banking, you don't need to repeat the work - they've already survived the 45-page gauntlet. If you actually talk to founders instead of processing them through a checklist built for small businesses, you learn what you need to know.

The banks that reject startups aren't doing it because they've assessed the risk and found it too high. They're doing it because they haven't built the capability to assess it at all, and at their cost structure, they never will.

That's not a regulatory constraint. It's a choice.

New companies with no revenue and offshore investors aren't going away. The infrastructure to serve them properly is long overdue.

Why Seapoint

We're building the financial infrastructure that startups in Europe should have had all along. A financial home that treats VC funding as a signal, not a red flag. That uses open banking to verify you've already passed KYB somewhere else, instead of making you start from scratch. That actually talks to founders instead of processing them through a checklist built for someone else.

If this sounds like what you've been looking for, join the waitlist.

What to know about fundraising: A founder's guide to running a tight process

Learn how to raise pre-seed to Series A capital efficiently. From preparation to closing, this guide covers the four stages every founder goes through.

January 29, 2026

Sean Mullaney

~5 minutes read

What to know about fundraising: A founder's guide to running a tight process

When we raised our €3M pre-seed, I thought I understood fundraising. I've been a Sequoia Scout, sat on boards, and watched dozens of founders go through the process. But doing it yourself? That's a completely different beast.

As a serial founder, the reality is you'll get 20 "no's" before you get 1 "yes." And those rejections will come at 8:30pm when you're exhausted in a hotel room after a day of back-to-back pitches.

This is the honest guide I wish someone had given me before we started, structured around the four fundraising stages every founder goes through: Preparation, Building Your List, The Roadshow, and Closing.

Stage 1: Preparation (3-4 months out)

Here's the first mistake: deciding to fundraise three weeks before you need capital. We started planning three to four months before kicking off. This wasn't overkill, it was necessary.

Start with your core message. A big early learning? Begin with the six-word description, the 20-word mission, the core nuggets you'll repeat 100 times. We did the long-form data room content first and tried to distil it down. Big mistake. Start with the essence, then expand.

Practice extensively before launching. Do practice pitches with every existing investor, get feedback, and iterate. Once you kick off the process, it's so intense that there's no time for major changes.

The golden rule: You need two years of runway from seed to Series A. For pre-seed, plan for 18 months to seed. But always subtract six months for your next raise.

Note on stages: Much of this advice applies whether you're raising pre-seed, seed, or even Series A. The mechanics stay the same, only the players and cheque sizes change.

Build your angel network early

Angels aren't just capital for your current round, they become infrastructure for everything that follows. What you're selecting for:

- Signal value: Can you say "former Google exec" or "founder of [successful company]" is backing you?

- Network access: Will they open doors to 4-6 quality VC intros when you raise your next round?

- Customer pipeline: Do they know your market and potential customers?

The angels you recruit during pre-seed become your warm intros to institutional VCs at seed and beyond. They're the references investors call. Think long-term.

Stage 2: Building your investor list

We built a list of 150 potential investors and immediately cut it in half by filtering out clear mismatches. Then we got to our core 40 top-priority targets.

Research checklist before you start:

- Cheque size compatibility: Can they write the amount you need?

- Stage fit: Look at their last 10 investments. If a fund has backed 30 companies at Series A and written two pre-seed cheques, they're not a great fit for your pre-seed round.

- Geography fit: Do they invest in European startups?

- Portfolio conflicts: Have they already backed a competitor?

- Fund status: Are they actively deploying?

- Decision timeline: Some firms can move to a term sheet in 48 hours. Others need three weeks minimum.

The pre-seed exception

At pre-seed specifically, there's value in taking some meetings with tier-one multi-stage VCs even though they probably won't invest. I used those early meetings as free consulting. The feedback I got led to a major revision of my investment memo. Then I refocused on smaller funds who actually write pre-seed cheques.

Just don't let these meetings dominate your calendar. Use them strategically for feedback early in your process, then move quickly to funds that actually write cheques at your stage.

Warm intros are non-negotiable

I'm going to be blunt: cold outreach is basically dead on arrival. But here's what surprised me: you don't need to know everyone personally before you start. We hadn't met many of our key angels before kicking off the process.

The hierarchy of intros matters:

- Founders and customers (best) - When a founder who fits your ICP introduces you, they're putting their reputation on the line. That signal cuts through.

- Angel investors and operators (good) - Often former founders who know the space.

- Other VCs (acceptable) - But they have skin in the game.

- Your own team (least credible) - Obviously, you'll talk yourself up.

A contrarian approach: "Licking the cookie"

Here's something most people will tell you not to do: I made my initial investment memo public. Not published on LinkedIn, but when I sent the Notion page to the first few angels, anyone with the link could read it.

What happened? People started forwarding it. Within a few weeks, 10-15 investors had reached out inbound. But the real benefit wasn't just the meetings. By getting the idea circulated widely in the VC community, I established territory. Even VCs who didn't back me knew I was solving this problem, which meant they were less likely to back a competitor who showed up six months later.

This won't work for everyone, but at pre-seed when you have nothing to lose, being open can be a competitive advantage.

Stage 3: The roadshow

VCs talk. Their associates live in WhatsApp groups sharing who's raising. Word got out within a week. This reality shaped our entire strategy.

Compress your timeline

We organised outreach in "waves" but these weren't weeks apart. Wave zero launched on a Monday. Wave one started Thursday. Wave two by the following Wednesday. Days, not weeks.

Why? Because momentum is a signal. When VCs hear you're talking to their competitors, they move faster.

When an intro email came in at 9am, we responded immediately with the deck and meeting link. When we agreed to send follow-up materials, they went out same-day. VCs read responsiveness as a proxy for how you'll operate as a founder.

Tactical tip: One founder I advise had their COO manage their inbox during the entire fundraising process. When intros came in, the COO responded within 10 minutes. This level of responsiveness became a signal to VCs that the team was organised and serious.

Use geography strategically

One tactical advantage if you're not based in a major funding hub: use that scarcity to your advantage. I'm not based in London, but I scheduled two weeks there for in-person meetings. On intro Zoom calls, I'd mention: "I'll be in London next week if you want to meet in person." This created natural urgency. Being an outsider became an advantage.

Watch for responsiveness

This is the single biggest signal of serious interest. Investors who are serious will respond quickly to intros, come back within their agreed timeframes, want to get follow-up meetings in the diary immediately, and ask for specific materials. If they're slow, they aren't serious. Full stop.

The emotional reality

Even when your raise is successful, no one prepares you for how depressing this process is. I did 70 meetings in three weeks. Week two is brutal because the rejection emails start flooding in, always late in the evening.

The way through this is process. Keep your pipeline moving. When you have 5-6 firms going to investment committee, you're statistically likely to get term sheets. Focus on the process, not the individual outcomes.

Another thing I've heard from founders who've raised multiple rounds: pre-seed actually feels less stressful than later stages. Why? Because at pre-seed, if you can't raise the capital, you simply don't start the company. So if you're reading this and paralysed by fear, you actually have less to lose than you think.

Here's what some founders get wrong: They think if they send one more piece of collateral, they can turn a "no" into a "yes." Stop. If there was critical missing information, the investor would have asked for it during diligence. Don't burn bridges in your responses to passes. Keep them short, polite, and professional.

Stage 4: Closing

When term sheets arrive

We were lucky to get multiple term sheets during our process. One actually had a higher valuation than the one we chose. But from the first call, I knew which firm was right. Trust your gut. This person will be on your board for years.

When you get a term sheet, don't shop around asking others to match the valuation. Instead, tell the firms still in process: "We have a term sheet. We're making a decision in five days. Can you reach a decision in that timeframe?"

You'll hopefully have 2-3 firms going to the investment committee in that final week. Remember: 80-90% of deals that reach IC get approved at most firms. But don't count your chickens, focus on having backup options until signatures are done.

What if you don't get term sheets?

Not every fundraising process ends with term sheets. If this happens, you have three options:

Reassess the fundamentals: Is the problem validated? Is the market timing right? Use the feedback from your conversations to identify what needs to change.

Pivot to a smaller round: If you were targeting £2-3M from VCs, consider raising £300-500K from angels instead. This gives you runway to build more traction.

Build without raising: Some businesses can get to early revenue without significant capital. If you can generate income from early customers, bootstrap to a stronger position.

Take a week to process with trusted advisors. Fundraising is a moment in time, not a final verdict on your company.

The right investor changes everything

All of this process talk might make fundraising sound transactional. It's not. When you find the right investor, it's one of the best things that can happen to your company.

The right VC brings pattern recognition from seeing your challenges play out across dozens of portfolio companies. They bring a network that takes years to build yourself. They bring credibility that opens doors. Most importantly, they bring genuine partnership, someone who'll take your 11pm "I don't know if this is working" call and help you think it through.

The process is rigorous, not because VCs are adversaries, but because finding the right match matters enormously. When you get it right, it's a multiplier on everything you do.

Here to help

Fundraising is intense, but with the right process and support, you can navigate it successfully.

At Seapoint, we work with early-stage founders across Ireland, the UK, and the EU. Our team includes experienced operators and former founders who've been through this process several times.

We run open office hours every Wednesday at 11am (in our London office and virtually). Whether you're preparing pitch materials, building your investor list, or setting up financial processes after your round, come talk it through with us. Fundraising is one of the most common topics founders bring to these sessions, and we're always happy to help.

Book a slot here.

Why financial clarity is the difference between survival and failure

Why most founders are flying blind on their finances—and how real-time visibility can mean the difference between running out of cash and reaching your next milestone.

January 8, 2026

Sean Mullaney

~5 minutes read

"The biggest thing that's going to kill a startup is not competition. It's probably that your idea isn't great - but also, you run out of money. So having the finance overview is so important."

That's what a founder told me during the research that shaped what we're building at Seapoint. Over the past year, I've spoken to 50+ European founders about their finances. The same frustration came up again and again: the people building Europe's most innovative companies are flying blind when it comes to their own financial position.

And here's what makes it worse - the problem doesn't get easier as you scale. It gets harder.

The spreadsheet that runs your company

When you're a three-person team, scrappy financial processes are fine. A Google Sheet, a folder of invoices, some mental arithmetic. But the moment you raise serious capital and start scaling, everything breaks.

"The source of truth is the Google Sheet where we pile it all together," one founder admitted. Another, running a team of 20+, described his investor reporting workflow: "I have to send this to the bookkeepers, they send me back a PDF report that I send to investors. In my mind, it's nonsensical - they're basically pulling it out of Sage, changing the format, slapping a logo on it and putting it into a PDF. I don't see why I can't just have a dashboard."

The pattern is consistent. Founders piece together their financial picture from multiple bank accounts, cryptic statements, and spreadsheets that grow more complex by the month. By the time you have a clear view of last month, you're already three weeks into the next one.

"If you end up having a three-week close period at the end of each month, you're always looking in the rearview mirror," another founder told me. "And that is bad, especially in a very rapidly growing business."

The scaling trap

Here's what nobody tells you: the faster you grow, the less visibility you have.

With five employees, missing a financial detail is embarrassing. With twenty-five employees depending on you making payroll, it's catastrophic. Yet the processes that worked at five people - the spreadsheets, the manual reconciliation, the quarterly check-ins with your accountant - those don't scale. They break exactly when the stakes are highest.

One founder captured the trajectory perfectly: "It's all very manual process, all that kind of crap. It's working for us right now, but we're totally in a scale phase. It's a headache now, it's going to be a migraine very soon, then it will turn into a full-blown implosion."

Another, who'd just raised a significant Series A, was equally direct: "What we don't have right now is good monthly reporting on accounting. It does live in Xero, but if we wanted to do a monthly P&L, it's still a little bit messy."

These aren't early-stage founders figuring things out. These are companies with millions in funding and dozens of employees, still flying blind.

Why your accountant can't save you

Here's an uncomfortable truth: most founders have never run a business before. They're not accountants. They don't have financial backgrounds. So when faced with the complexity of managing company finances, many just throw it over the wall, "That's the accountant's problem."

But your accountant can't actually solve this. They're essential for compliance, including tax returns, statutory accounts, and ensuring you're legal. But they're not set up for real-time operational visibility. They work in monthly or quarterly cycles, not the daily reality of running a scaling business.

"I hate logging into Xero," one founder told me bluntly. "It's kind of useless to be honest, aside from just looking at bank balances."

The tools accountants use, such as Xero, Sage, and QuickBooks, were built for accountants. They're designed around compliance and categorisation, not the real-time decision-making that running a startup demands. Your accountant gets what they need. You get PDFs three weeks after the fact.

Meanwhile, your financial stack multiplies. One founder laughed ruefully: "Our fractional CFO has concocted a financial stack more complex than the product we're trying to build."

The hidden cost of not knowing

The consequences of financial blindness aren't abstract. They show up in very concrete ways.

"I feel like we're just paying so much on random software subscriptions, but it's really hard to find out," one founder confessed. Without visibility, forgotten subscriptions and unused tools quietly eat away at runway. That €200/month analytics tool nobody uses? It adds up to €2,400 per year—and most founders have several of these lurking in their expenses.

Another founder preparing for fundraising shared his experience: "When it came to fundraising, the biggest challenge was building a budget or forecast. I had no idea how. I knew what I was spending each month, but not where it was going or how to project it forward."

This is the cruel irony. At the exact moment you need financial clarity most - when you're raising, when you're scaling, when you're making critical hiring decisions - your financial picture is at its messiest.

And here's the psychology that makes it worse, many founders respond to this anxiety by sticking their heads in the sand. They know they should be on top of their finances, but because it's something they're not naturally good at, they avoid it. "We've just raised, there's plenty of money in the bank, I don't need to worry about this right now." Until, of course, it's too late. The founders who get into trouble aren't stupid or careless. They're human. They avoided the thing that scared them until avoidance was no longer an option.

What we're building

Every founder I spoke to described the same wish: "We want an active view of the business. It's just a manual process for us right now, we'd love someone to just go in and be able to do that."

This is exactly what we're building with Seapoint.

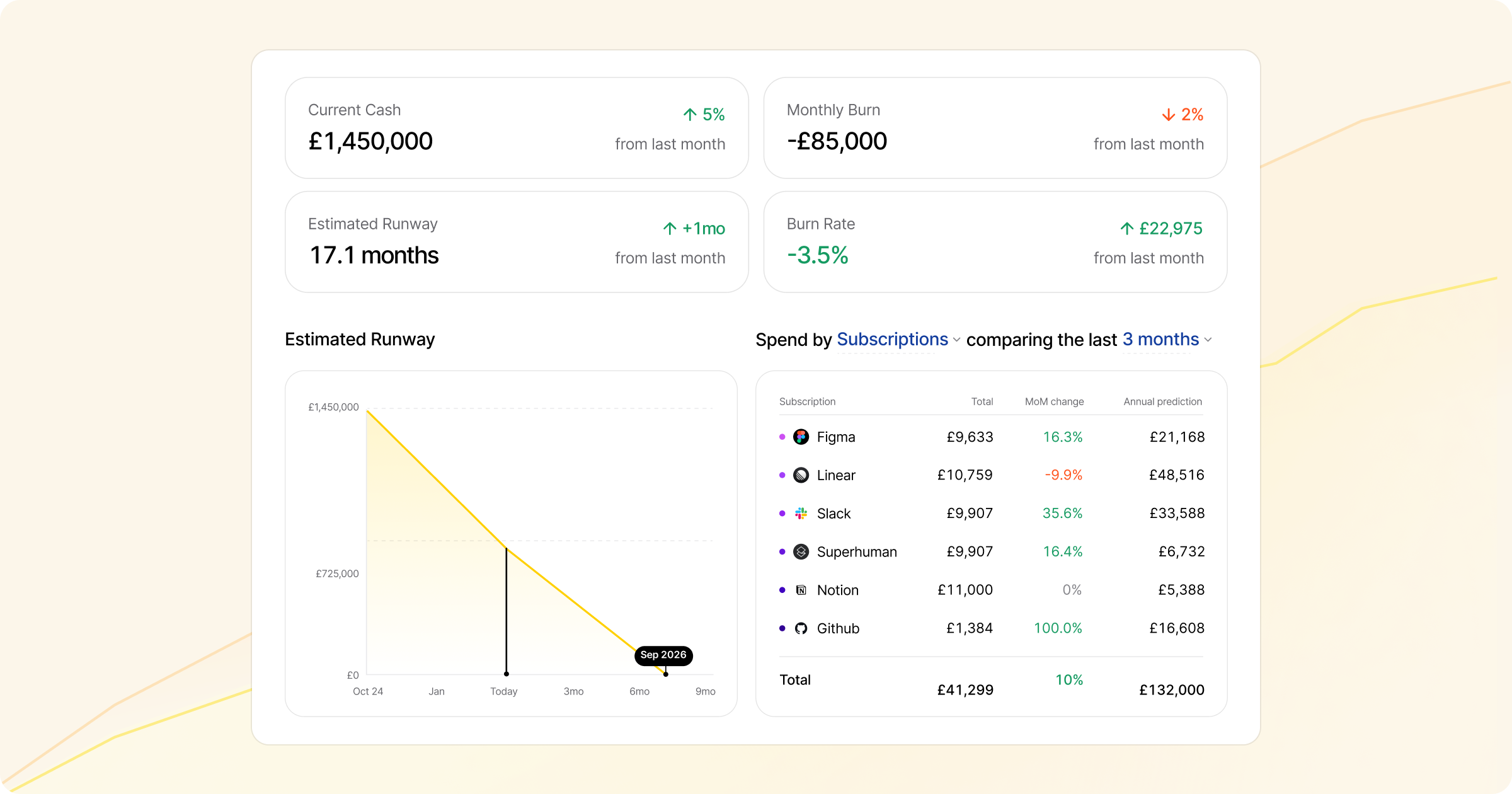

We connect all your bank accounts, across currencies, across entities, and unify them with your accounting data. Within minutes of connecting, you have a real-time view of your complete financial position. No spreadsheets. No waiting for your accountant. No three-week delays.

Our AI automatically categorises transactions, flags anomalies, and surfaces the insights that actually matter: that subscription you forgot to cancel, the vendor whose invoices have quietly increased 40% over six months, the burn rate trend that needs attention before it becomes a crisis.

The result is simple: you can answer "what's our burn rate?" or "how much runway do we have?" in seconds, not days. You can walk into a board meeting or investor call knowing exactly where you stand.

And because we built Seapoint as a complete financial platform, not just a dashboard, you can also pay invoices, run payroll, and manage expenses in the same place. One login. One view. One source of truth.

Why this matters

I've been a founder multiple times. I've lived the anxiety of not knowing exactly where the cash stands, of making decisions based on gut feel when the stakes are highest.

Running out of money is still the number one reason startups fail. The founders building Europe's future deserve better than spreadsheets and stale PDFs. They deserve to know, in real-time, exactly where they stand.

That's what Seapoint delivers.

We're currently in private beta. Within minutes of connecting your accounts, you'll have the financial clarity that used to take weeks. Join the waitlist here, we're onboarding new companies every week.

Subscribe to our newsletter

Get practical resources and insights for ambitious startups straight into your inbox.